Jon - Trident Home Loans

Super User

-

Joined

-

Last visited

Everything posted by Jon - Trident Home Loans

-

Good news before 2022 PCS season…Fannie Mae and Freddie Mac raised the normal lending threshold today on conventional loans by almost 99k to $647,200. There are higher limits for expensive counties like those in the DC area. This mean you can borrower more at lower rates without needing a jumbo loan. The VA will certify these new limits soon too which means you can borrow more before it becomes a high balance VA loan which keeps your rate lower. It also helps people looking to get a second VA while keeping one they have on another property because VA entitlement is calculated off these numbers too. Basically you’re getting another 99K of VA insurance. No change to entitlement if your entitlement is fully available…you can still go zero down without a loan limit assuming you qualify debt to income ratio wise. Let me know if we can do anything for you or if there are any questions I can answer. Happy Holidays! Jon 850-377-1114 jk@mythl.com

-

Assuming its a VA loan then it'd just be a normal VA High Balance loan. VA doesn't have the jumbo rate penalty like conventionals. High balance loans rates are typically only .125-.25% higher than a conforming loan (loans below 548,250). For 2021 the conforming transition point is going up to 625K. We've already gone up to the new limit for conventionals but VA likely wont start until the VA announces it in Dec. My assistant Lisa has our MD license so she'd be the one to do the loan for you. You're welcome to reach out to her at 781-710-9675 or at lisa@mythl.com to work a preapproval/talk rates. Cheers! Jon 850-377-1114 jk@mythl.com

-

Thanks man and congratulations! Love helping and getting those great deals out! Perfect timing on your part. Had a little rate bump last Thur after the Federal Reserves announcement but everything is settling down so hopefully lots more good deals to come for those PCSing this winter or wanting to refi. Still seeing us killing the competition so even if the overall market moves higher we will be in a great position to help. Jon

-

No issue if it’s a spouse. Not going to happen if it’s not a spouse. Technically the VA allows it but it has to go to the VA for approval at the end and usually gets shot down. We don’t even start them because of the drama at the end. You could add the person to the deed after closing as a work around. Wouldn’t be able to use their income or have them on the note/deed at closing. Feel free to call me if you want to talk about it more. Jon

-

-

Glad to hear you're happy and thanks for the shout out! It was a pleasure working with you and glad we got to save you some money! For anyone in a conventional loan, Fannie Mae and Freddie Mac just dropped the adverse market fee they were adding to conventional refi rates/pricing that was artificially jacking up rates. Basically seeing .125-.25% less on conventional refi rates as a result. Jon

-

Lender credits are basically reverse points. When a rate makes us above our profit margin we just give it back to our clients to help them with their closing costs. Right now our par rate of 2.25% on VAs below $548,250 on purchases is paying extra so we're able to give a credit usually at it. If that credit isn't enough we can look at higher rates that make us more and then pass that along in the form of a larger lender credit. Closing costs vary from state to state (transfer taxes, title costs, recording fees to the county, etc) FL and VA are more expensive to close in vs TX as an example. Lenders' profit margins all vary so finding the lender with the lowest undiscounted base rate will set you up for success in getting larger lender credits. I do a lot of loans with zero closing costs by finding a rate that covers all the cost. It's all breakeven math to see what rate/credit combo makes the most sense based on how long you'll own the house. If you're only owning a house for 3yrs and you get a 5K lender credit for only $90 a month more in interest then you have 55 payment breakeven which is longer than the 36 months you'd own the house. Hope that makes sense. Feel free to call me if you want to chat through it more. Jon 850-377-1114

-

Since we're not a bank we have to be individually licensed in every state. Some have requirements to have a physical branch location in the state while others just have some significant red tape. We're down to just 5 left with NY being one of them. It's just a paperwork game with NY but the plan is to get all 50 states eventually. I don't have any good contacts up there to recommend unfortunately...just don't want to steer you wrong since I don't personally have any experience with anyone there. If you'd like me to ask some of our business contacts for recommendations I'd be happy to do that. Just drop me an e-mail at jk@mythl.com. Jon BTW VA rates are still great right now on both purchases and refi's. Getting pretty much everyone 2.25% with no discount points or lender fees and even lender credit on loans below 548,250. Haven't seen anyone quote where we are at so to my knowledge we should be one of the most competitive lenders out there on VA loans.

-

-

Fannie and Freddie are limiting their second home and investment property exposure to 7% of their portfolio which has pushed rates up/pricing down in the secondary market. Some investors still have great pricing because they weren’t overexposed so it’s definitely something you need to shop around for when you go to lock. Since we have multiple investors we shop around for you behind the scenes so we can always offer the best pricing. Careful of lending tree because their cut is built into the lender’s rates/fees. You want to go direct as much as possible to avoid hidden costs. I can’t give you generalized second home rates without know the specific numbers/transaction details. Feel free to reach out and I’ll give you the best advice I can. Jon

-

Thanks man! Hopefully this is your last one for a while! It’s been great working with you over the years! Let me know if you ever need anything. Lots of realtors trying to get people to go conventional over VA even though I’d argue VA is more flexible, better deal, and faster closing. Some agents are stubborn and won’t hear it but I’ve had good luck educating both buyers’ and sellers’ agent by leveraging my VA lending credibility. Big thing is VA appraisals come in much faster. The old wives tale that a buyer can’t pay over appraised value on a VA isn’t true. It’s the buyers decision upfront or when the appraisal comes back and you can write an appraisal gap into the contract. That’s usually the biggest VA sticking point. Rates will go up when the fed curbs their bond buying to fight inflation but for now we’re still doing purchases in the 2.25-2.375 range without discount points or lender fees for both regular VAs and jumbo VAs. Let me know if I can do anything for anyone. Jon 850-377-1114 jk@mythl.com

-

We don’t do HELOCs or home equity loans. We do cash out refi’s. Lots of different rules on those depending on type of loan and residency. VA’s are best but only can do on a current primary residence. Can go up to 90% loan to value but the VA funding fee is steep at 3.6%. Best combo is VA disability to exempt people from the funding fee and a VA cash out. Conventional primary’s are capped at 80% and 2nd home/investment at 75%. Interest rates are also higher on conventionals then higher on conventional 2nds and investments. VAs are always the lowest rates. It can be hard to get a HELOC on a second home/investment property so best to open them while they are your primary. Those are going to be a bank or credit union product. Give me a ring or email if you want to talk through specifics. 850-377-1114, jk@mythl.com Jon

-

Thanks man! Ya that was a crazy closing scenario! Props to you for keeping your cool and working through all the crazy weather/logistical issues. We’ll always work our butts off for guys like you who have a great can do attitude! I laugh when people hunt around to save $15 a month or realtor says you need to use a “local lender” thinking that buying a home or getting a loan is some turn key event. Great customer service and working with people you can trust is critical when the going gets tough...title, lender, realtor alike. You definitely deserve that beautiful home! Enjoy living in base and the flying! I’m back to flying/commuting in Jun. Jon jk@mythl.com 850-377-1114

-

Thank you! Thanks for the nice words and congrats on the close! Appreciate you trusting us with your business and helping others find us I just had a loggie in Cali call yesterday for a 700K high balance VA loan purchase. A very large bank that sponsors everything military related was quoting 3.125% and we've been at 2.375%. He heard about us through 2 AF friends who had both closed with us. Old school word of mouth definitely still works. Cheers! Jon

-

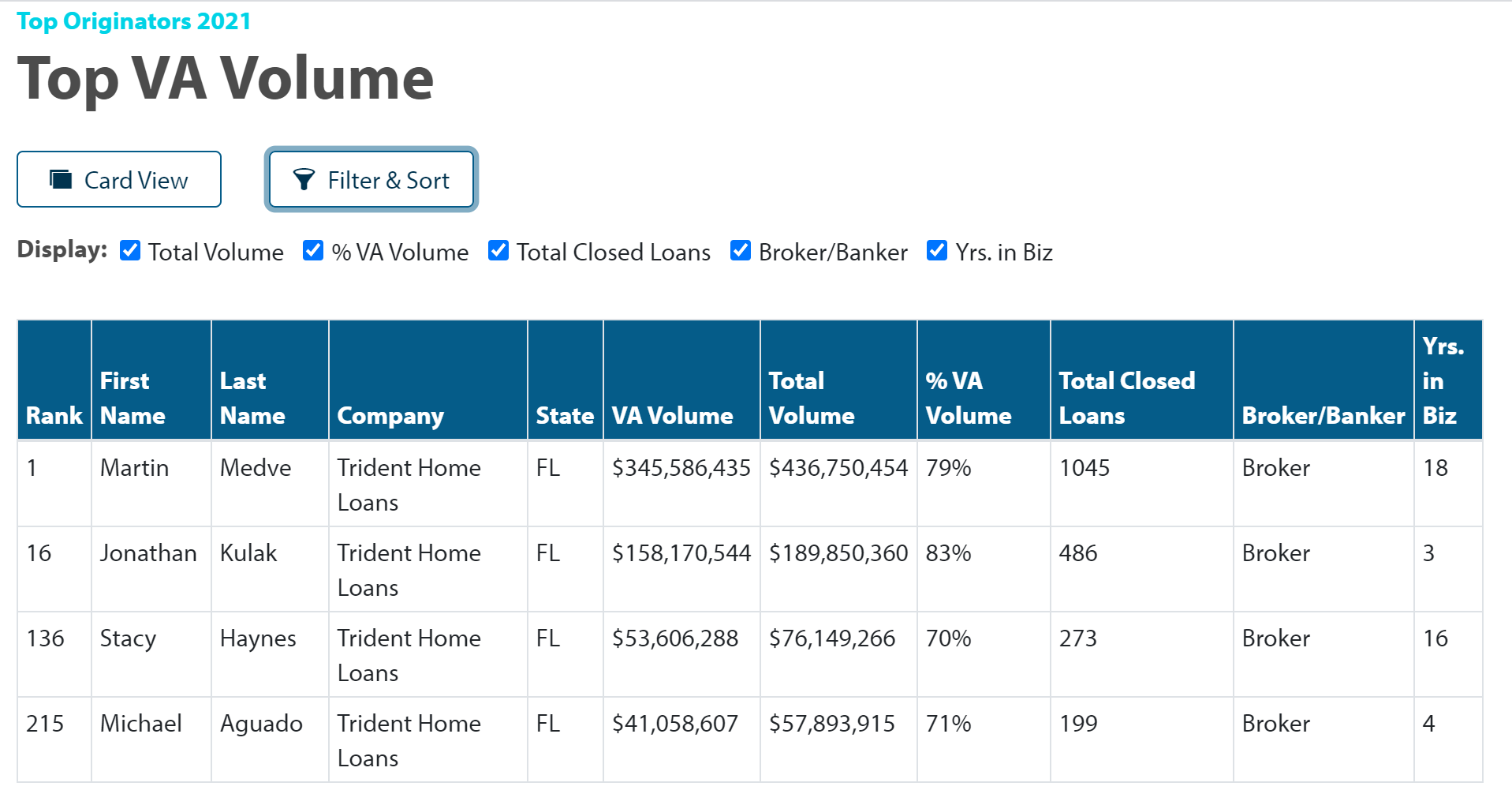

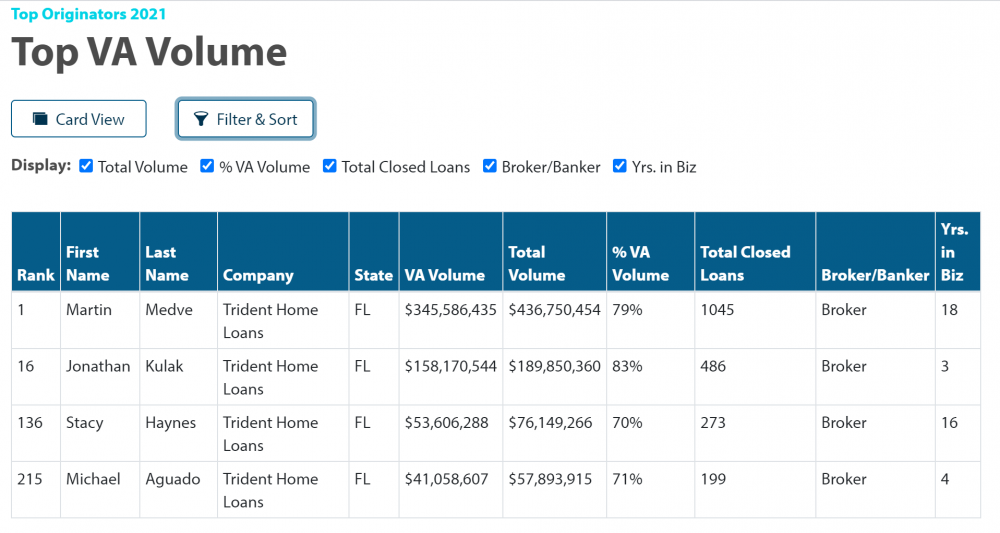

On behalf of Marty and everyone at Trident Home Loans we wanted to say thank you for promoting us around the AF! We don't spend a dime on advertising and everyone who has done business with us has helped Marty our owner rank as the #1 VA loan officer in the country for 2020 and even got me to #16. That being said Marty says if you're not first you're last...neither of us even knew they made 16th place ribbons In all seriousness though we really got our grass roots start on Baseops and it has just spread the old school way. These rankings just help us help all our clients leverage the best VA loan rates/pricing out of Wall Street and also give us some extra credibility when we call listing agents on your behalf! Thanks again and know we're always here for you! Cheers! Jon 850-377-1114 jk@mythl.com Application Link Rankings Source

-

Thank you! Happy to be able to do it! You got in at a perfect time. These rates won't last forever. Today was the first day in a while that Wall St started going the other way in the bond market which then negatively impacts mortgage rates. Nothing crazy and rates are still insanely low but just a reality check that there will be a correction at some point. Jon

-

Thank you so much and congrats! We always have everyone’s back! We don’t work for referrals from realtors, title companies or anyone else who stand to gain from shady deals. We are 100% for our clients’ interests and I’ll be the first to destroy anyone who cause problems for you. If I can’t get my will done then Marty will. Usually it doesn’t come down to that but sometimes we need to flex a little...I don’t know if they heard us counting but we did over 100😉 Jon

-

-

Get with a local bank or credit union for an interest only portfolio construction loan. Once you're about 30-45 days out from the house being done we'll start the permanent VA loan. It'll be a VA cash out refi so it's capped at 90% loan to value to include the VA funding fee. Highly recommend getting VA disability first if you don't have it already to avoid the 3.6% funding fee. Jon

-

Thanks gents! Sorry for being slow to reply...for some reason notifications aren't coming through but I hop on every few days to check in. It was a pleasure helping all of you out! Thanks for spreading the word about Trident! Looking forward to helping a lot more of you guys this year! For an immediate response make sure you're calling, texting or emailing me. We expect rates to stay low for a while but finish the year slightly higher. Jon 850-377-1114 jk@mythl.com

-

Good news...we can now lock based on the new VA limits for 2021 which raised the jumbo transition limit to $548,250. Our jumbos and non-jumbos are both at 2.25% no points, no lender fees but we're able to give a nice lender credit on the non-jumbos especially in the higher loan amounts. Have a great Christmas! Jon 850-377-1114 jk@mythl.com

-

Interest rate gets locked when you go under contract. A preapproval is good for 120 days because that's how long a credit report is valid. The credit report needs to be good through the closing date so if it's going to expire then we just need to refresh it. We're doing all our 2.25% VA refi's with no points and no lender fees plus a lender credit. If someone is trying to charge you points or origination fees then you're getting a bad deal. You can close on a new VA refi 210 days after making your first payment so you're coming into that window. I'd just have to look at the third party costs, lender credit available, and your loan amount to see if it's worth going down just .5%. On big loans or if we can do it for free then definitely but on smaller loans or if it's in an expensive refi state like FL then probably not worth it. Happy to take a look at it for you through. Jon

-

Not sure I understand the question? Rates aren’t locked in until you go under contract to buy a house. We don’t charge any fees so any difference in the APR vs rate is the VA funding fee and any settlement fees charged by the title company. If you’re exempt from the funding fee and you don’t pay a settlement fee with the title company then 2.25% would be 2.25% APR. APR isn’t a thing in our world really because we don’t charge any fees to our clients

-

Thanks Sir! We try out best. Rates/pricing are awesome thanks to you guys doing business with us. Our loan portfolio is highly sought after by big money investors because of the high quality borrowers/loans we sell (that’s how we make our money on backside of the transaction). No only do we get to work with great fellow servicemen/women but you are why we get special pricing incentives that no one else in the country gets. That in turn comes back to you guys as in the form of lowest rates, no lender fees, and lender credits when able. It’s an awesome circle and we only have all of you thanks. Keep spreading the word and it’ll come back to every vet who works with us. Jon

-